How To Get Capital One Student Credit Card In 2022

A student credit card is a great first step in establishing a good credit history. Building good credit card history might not seem like a priority when you’re still in school, but you’ll need it down the road if you want to finance a car, buy a house or qualify for the best credit card offers. Your credit card history can even affect your job prospects and your ability to rent an apartment. When it involves making smarter financial decisions, Capital One is one brand that offers a full suite of student credit cards with enough rewards and benefits to make any student credit card holder in 2022 feel like a real adult on their journey of credit limit building. In this article, we will be discussing How To Get Capital One Student Credit Card In 2022.

Capital One Student Credit Card At A Glance

For a long time, Capital One’s Student Rewards card was positioned as a beginner credit card for students trying to build credit limits, and it was the issuer’s only such product. However, there is a student credit card for two of its other student credit cards.

Capital One SavorOne Student Cash Rewards Credit Card:

Rewards rate: 3% cashback on restaurants, entertainment, popular streaming services (such as Hulu, Disney+, and Netflix), and grocery stores (excluding superstores such as Walmart and Target);

8% cashback on tickets purchased through Vivid Seats through January 2023;

All other purchases are subject to a 1% surcharge.

Welcome offer: N/A

There is no annual fee.

APR: 26.99 percent changeable regularly

Capital One Quicksilver Student Cash Rewards Credit Card:

Rewards rate: 1.5 percent cash back on all purchases

Welcome offer: N/A

Annual fee: $0

Regular APR: 26.99 percent variable

Journey Student Rewards from Capital One:

Rewards rate: When the card is paid on time, the cashback is increased to 1.25 percent on all purchases for the month.

Welcome offer: When you pay on time, you can get up to $60 in monthly streaming service credits (must be earned within the first 18 months)

Annual fee: $0

Regular APR: 26.99 percent variable

Similarities Between Capital One Student Cards:

The Quicksilver Student Cash Rewards and SavorOne Student Cash Rewards, two of the newest Capital One’s student credit cards, are the most similar. However, there are a few things that all three cards have in common.

Rewards Redemption:

Cardholders of the Quicksilver Student and SavorOne Student cards can utilize their cashback earnings to get statement credits, pay using PayPal, shop at Amazon.com, and even get gift cards from retailers including Walmart, Lowe’s, and Whole Foods.

Card Network Benefit:

As part of the Mastercard network, Quicksilver Student and SavorOne Student credit cards also receive various benefits, such as cellphone protection, price protection, extended warranty, complimentary concierge services, rental coverage, roadside assistance, and ID theft protection.

Credit-building Features:

If you’ve used your card properly for the past six months, you’ll be eligible for a credit limit increase with any of these cards. CreditWise credit monitoring is available to all Capital One student credit cardholders.

Interest And Fees.

These three Student Credit cards all offer the same variable interest rate and no annual fee.

Differences between Capital One Student Cards

Each of these Capital One student credit cards has its own set of incentives. The Journey Student Rewards card is also a Visa, not a Mastercard, which means it has a separate set of benefits for cardholders.

Rewards Rate:

The only difference between these Capital One Student credit cards is the reward rates. The SavorOne Student credit card has greater rewards rates in specific categories, but the Quicksilver Student and Journey Student have (different) flat rates across the board.

Card Network Perks:

Another distinction is that the SavorOne Student and Quicksilver Student are Mastercard cards, whereas the Journey Student is a Visa card. As a result, the advantages are a little different. $0 fraud responsibility, virtual card numbers from Eno, and emergency card replacement are just a few of the benefits that come with the Journey Student. These Capital One student credit cards are ready to offer some beneficial and lucrative student credit card benefits, whether you’re a new college student, a graduate student, or even an overseas student.

These Student credit cards also contain student-friendly benefits like no annual fees, no international transaction fees (if you study abroad), credit monitoring, and improved conditions for responsible credit use, all of which can help you save money on your student budget. On the other hand, you can start with a lower credit limit and a higher interest rate.

What To Consider When Choosing A Student Credit Card:

1. Credit Reporting:

TransUnion, Experian, and Equifax should all receive reports from the student credit card you choose. These businesses collect the data that is needed to construct credit scores. That’s why you want them to keep track of your solid payment history. Except for the Deserve® EDU Mastercard for Students, which claims it reports to Experian and TransUnion, all other student credit cards report to all three bureaus.

2. Annual Fee:

When you’re on a student budget, avoiding an annual charge is excellent. A no-annual-fee student credit card not only keeps prices low but also makes it easier to keep an account open if you’ve built up enough credit limit to move on to better credit cards. You can keep your original student credit card open without paying an annual fee to extend your credit card history and improve your credit limit.

3. Interest Rates At The Start And Over Time:

Because student credit cards created for those who are new to credit have higher interest rates, it’s preferable to pay your account in full each month to prevent paying interest. Some student credit cards, on the other hand, provide an introductory 0% interest term, which might be useful if you have a large purchase to make you’ll need a few months to pay off.

4. Rewards:

Look for a Capital One student credit card that offers a rewards rate of at least 1% if you want to earn points or cashback for your purchases. Some student credit cards are more generous than others, but 1% is a good starting point. If you choose a Capital One student credit card with incentives that match your purchasing habits, you’ll receive more value for the money. A sign-up bonus is also available on some student credit cards.

These benefits may help alleviate the cost of your education expenditures, but only if you don’t go overboard to obtain them. If you do decide to get a student credit card with incentives, only use it for things that are already within your budget.

5. Foreign Transaction Fees:

Surcharges on purchases made outside the country, usually ranging from 1% to 3% of the entire transaction value, are known as foreign transaction fees. If you’re spending a full semester in a study abroad program, this can be a significant financial burden. Look for a student credit card that doesn’t charge foreign transaction fees if you plan to travel outside the United States. Discover and Capital One, for example, don’t levy these fees on any of their student credit cards.

6. International Acceptance:

Another thing to think about when studying abroad is how easy it will be to use your student credit card. Visa and Mastercard are commonly accepted throughout the world, but American Express and Discover are not.

Advantages Of Students Credit Card:

When you’re still in school, building a credit limit may not seem like a top priority, but the sooner you start building your credit card history, the better. Having a high credit limit will help you buy a house or secure a vehicle loan in the future, but there are even more immediate benefits. A good credit card history, for example, can help you get a job or rent an apartment.

1. Credit History:

Your credit card history is detailed in your credit report, which is summarized by credit ratings, which indicate how well you’ve managed borrowed funds. One of the quickest and easiest ways to improve credit limits is to use a student credit card properly.

2. Borrowing Money:

Good credit card history might mean the difference between approval and rejection when applying for a student credit card, car loan, personal loan, mortgage, or other loans. Furthermore, having good credit card history may entitle you to reduce interest rates, which saves your money.

3. Renting An Apartment:

When you apply to rent an apartment, the landlord may demand your credit report to see if you’re likely to pay your rent on time.

4. Setting Up Utilities:

Customers’ credit card histories are routinely checked by utility companies. If you have poor or no credit card history, your electricity company or water provider may request a deposit or a letter of guarantee from someone who agrees to pay your payment if you can’t.

5. Getting A Job:

You may need strong credit card history to pass a job screening, depending on your profession. Credit limit checks are done by some employers, especially for professions that require handling other people’s money.

6. Starting A Business:

When you’re looking to create business credit, some creditors look at your personal credit card history. If you want to start a business or keep the door open to the possibility open, a good credit score can help you keep interest rates affordable.

Eligibility Criteria For Capital One Student Cards:

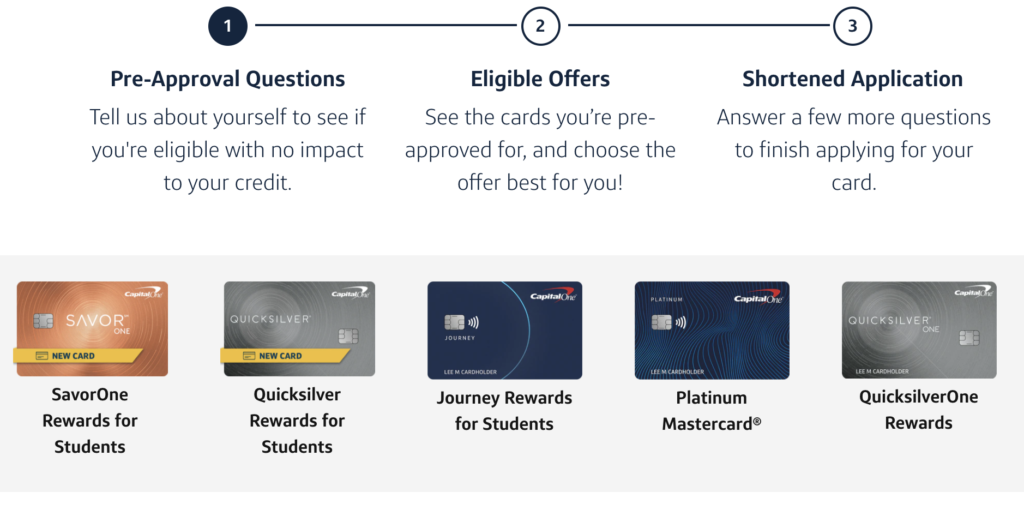

Capital One student credit card encourages wise spending by giving cardholders 1% cashback on all purchases. Pay on time to increase your cashback to 1.25 percent for the month. Start by looking into “pre-qualified” or “pre-approved” student credit card offers you receive in the mail or online. When you see one of those terms, it usually signifies that your credit card limit and other financial information met at least some initial requirements for obtaining a student credit card.

To determine if you’re pre-approved for a Capital One student credit card, you can utilize Capital One’s pre-approval tool. Pre-approval has no bearing on your credit score, so it’s a good way to compare options and find the best fit. Being a college student, on the other hand, isn’t enough to qualify for a student credit card. Here’s everything you need to know about it.

1. Student Status:

This may (or may not) be significant. For application eligibility, check the card’s terms and conditions on the issuer’s website. For example, the Capital One Journey Student Rewards program has no stated student requirement, whereas the Discover it Student Cash Back program‘s terms state, “You must be a college student.”

2. Federal Regulations:

In the United States, federal rules restrict who can obtain student credit cards if they are under the age of 21. Issuers are not allowed to give student credit cards to anyone under the age of 21 unless they have proof of independent income or a co-signer, who agrees to be responsible for the debt if the principal cardholder fails to pay the payment. Because most major student credit card providers do not allow co-signers, this can be a stumbling obstacle. Those aged 21 and up must additionally present proof of income. They can, however, disclose any income that they have a “reasonable expectation of access” to.

3. Bad Credit Is Usually A Dealbreaker:

Student credit cards are for persons who have very little or limited credit card history. You won’t be able to get a student card on your own if you have negative credit due to missed payments or other mistakes. In such a scenario, consider a card developed exclusively for those with a weak credit limit.

What To Do If You Don’t Meet The Eligibility Criteria for Student Cards:

If You’re Under The Age Of 21 And Can’t Meet The Requirements On Your Own:

You can have a parent add you to one of their cards as an authorized user. Authorized user status can aid in the development of a credit card history. You’ll get a card with your name on it that you can use to make purchases, but the debt is technically your parent’s responsibility.

If You’re Over 21 And Still Have Trouble Qualifying:

Even if you have a full-time job, if you don’t have a credit card history, it can be difficult to qualify for a normal credit card. Even better, secured credit cards are a fantastic option. They’re easier to get because they need a security deposit, which decreases credit card issuers’ risk. Use one to establish a credit limit, then upgrade to a better card.

If you are unable to overcome any of these obstacles and wish to begin developing a credit limit, you should, some rent-reporting firms will charge you a fee to record your rent payments to credit bureaus. It may be less expensive than putting down a deposit on a secured credit card. Being able to demonstrate a strong payment history could even help you qualify for a credit card in the future.

If You’ve Already Established Credit And Have Independent Income:

Consider skipping student credit cards entirely if you’ve previously built a credit limit and have a steady source of income. You might be eligible for a capital one student credit card with better benefits, a larger sign-up bonus, or cheaper interest rates. If you don’t yet fulfill the requirements for these capital one student credit cards, you can expect to have them once you’ve established a good credit limit.

How To Use Capital One Student Credit Cards:

You’re ready to start building a credit limit once you’ve been authorized for a capital one student credit card. Here’s How To Make The most of your card:

1. Only Purchase What You Can Afford:

When you don’t have the cash on hand to cover a night out with pals, it can be tempting to charge it. However, if such spending becomes a habit, it can lead to financial ruin.

2. Pay On Time And In Full Every Month To Avoid Interest.

Use your capital one student credit card to create good credit card history rather than to spend money you don’t have. To keep your card’s grace period in effect, use it for little purchases that you can afford to pay back on time and in full each month. You’ll keep track of your spending and save money on interest. Pay more than the minimum if you can’t pay your entire balance. If paying your entire sum isn’t possible, at the very least pay more than the minimum amount due. You’ll be able to make more progress toward paying off your debt.

3. Use Only A Portion Of Your Available Credit.

Your capital one student credit card may have a $1,000 credit limit, but it’s not a good idea to use the entire $1,000. Maintain a good credit utilization ratio and safeguard your credit rating by keeping your debt under 30% of your credit limit. As a student, you’re unlikely to receive a big credit limit, so keep your card for minor expenditures.

4. Be Strategic With Your Sign-up Bonus And Rewards:

If your student credit card comes with a sign-up bonus, structuring your application around expected expenses will help you achieve the bonus requirements without having to spend more money. Selecting a student credit card with incentives that correspond to your expenditure will also benefit your wallet.

5. Keep Your Account Open If Possible:

Keep your capital one student credit card open if it doesn’t have an annual fee to keep your credit card history and credit score intact. Closing a student credit card can damage the credit score you’ve worked so hard to get. Last but not least, keep in mind that when you’ve established a good credit card history by appropriately using your student credit card, your lender may consider raising your credit limit.

These Capital one students’ credit cards may be a suitable alternative for you if you want to earn rewards but prefer the security of a lower credit limit and no annual fee. When compared to other student credit cards, the continuing APR is somewhat high, but if used carefully, students can avoid high-interest costs by paying down their balance in full each month. Generally, either of these Capital one student credit cards could be a good place to start for students who want to receive rewards while building a credit limit.

You should be aware that simply being a college student may not be sufficient to qualify for a Student credit card. You’ll almost certainly require proof of income, and if you have a bad credit history or none at all, getting accepted may be difficult. Consider a secured student credit card in that instance. You must put down a cash deposit as collateral for these cards. The deposit protects the issuer if you do not pay your bill, lowering the risk of issuing you a card.

Conclusion:

It’s as much about the credit as it is about the card. Perhaps the most significant benefit of a student credit card for college students is the credit they can establish with it: good credit card history(when used responsibly, of course). Paying your credit card bills on time every month is part of being a responsible credit card user.

So seek a card with features that will assist students and first-time consumers in developing a positive credit connection. These cards may have educational resources and features such as credit-tracking software that can assist children to learn how to utilize credit responsibly.

Frequently Asked Questions:

So, Is Getting A Student Credit Card The Best Option?

Credit card ownership is, without a question, a significant step. However, because good credit takes time to acquire, many students find it advantageous to begin early. And assisting a student in selecting and learning how to use their first credit card might be beneficial after they graduate and enter the workforce. Consider the opportunity to establish a strong credit card history as yet another vital lesson in addition to the degree they’re pursuing!

Which Capital One Student Credit Card Should I Use?

Each student’s credit card is matched to a specific set of financial objectives and spending habits.

What Student Credit Cards Does Capital One Offer?

The Capital One SavorOne Student Cash Rewards card is designed for “food and leisure” expenditure and rewards you with different cashback categories. The Capital One Quicksilver Student Cash Rewards card includes many of the same features and benefits as the SavorOne student credit card, with the exception that the flat-rate cashback for all spending is set at 1.5 percent.

With on-time payments, the Journey Student Rewards program gives a fixed 1% cashback, which can be increased to 1.25 percent. If you use streaming services, the welcome bonus credit may be able to assist you to save money on those as well if you pay on time.

Are Capital One Student Cards Worth It?

Any of these Student credit cards could be useful if you’re a student looking to start boosting your credit limit while receiving incentives. Capital One designed these card suites specifically for students, recognizing that their income and credit profiles will be limited. Because the acceptance probabilities are based on your demographic, you’re more likely to get approved for one of these cards than for traditional rewards or cashback credit cards.

COPYRIGHT WARNING! Contents on this website may not be republished, reproduced, redistributed either in whole or in part without due permission or acknowledgment. All contents are protected by DMCA.

The content on this site is posted with good intentions. If you own this content & believe your copyright was violated or infringed, make sure you contact us at [xscholarshipc(@)gmail(dot)com] and actions will be taken immediately.